Financial statements are the vital signs of your business, and knowing how to read financial statements as a small business owner is the single most direct path to sound fiscal management. The three core reports, the income statement, the balance sheet, and the cash flow statement, each reveal a different dimension of your financial health. You do not need CPA-level expertise to use them well. You need a disciplined reading habit and a clear understanding of what each number actually means. This guide gives you both.

What are the three primary financial statements?

Every small business produces three primary financial reports. Each one answers a different question about your business.

| Statement | What it shows | Time frame |

|---|---|---|

| Income Statement | Revenue, expenses, and net profit or loss | A period (month, quarter, year) |

| Balance Sheet | Assets, liabilities, and owner’s equity | A single point in time |

| Cash Flow Statement | Actual cash in and out of the business | A period (month, quarter, year) |

The income statement acts like a movie. It plays out your financial performance over a set period, showing every dollar earned and every dollar spent. The bottom line is net profit or net loss. That number tells you whether your business model is working.

The balance sheet is a snapshot taken at one moment in time. It lists everything your business owns (assets), everything it owes (liabilities), and what is left over for you as the owner (equity). The fundamental accounting equation holds it together: Assets = Liabilities + Equity. If that equation does not balance, something is wrong in your books.

The cash flow statement tracks actual cash movement across three categories: operating activities, investing activities, and financing activities. Operating cash flow is the most telling number for a small business. It shows whether your core business generates real cash, not just accounting profit. A business can show a profit on the income statement and still run out of cash. The cash flow statement is where that gap becomes visible.

How to analyze financial statements for a full picture

Reading one statement in isolation gives you an incomplete view. Reading all three together is where the real analysis begins. The most common trap is seeing a healthy net income on the income statement and assuming the business is fine. If cash flow from operations tells a different story, you have a problem worth investigating.

The gap between profit and cash is one of the most reliable early warning signs in small business finance. Slow-paying customers, inventory buildup, or prepaid expenses can all create a situation where your income statement looks strong while your bank account shrinks. Experienced advisors consistently point to this gap as the first place to look when a business feels financially tight despite reported profits.

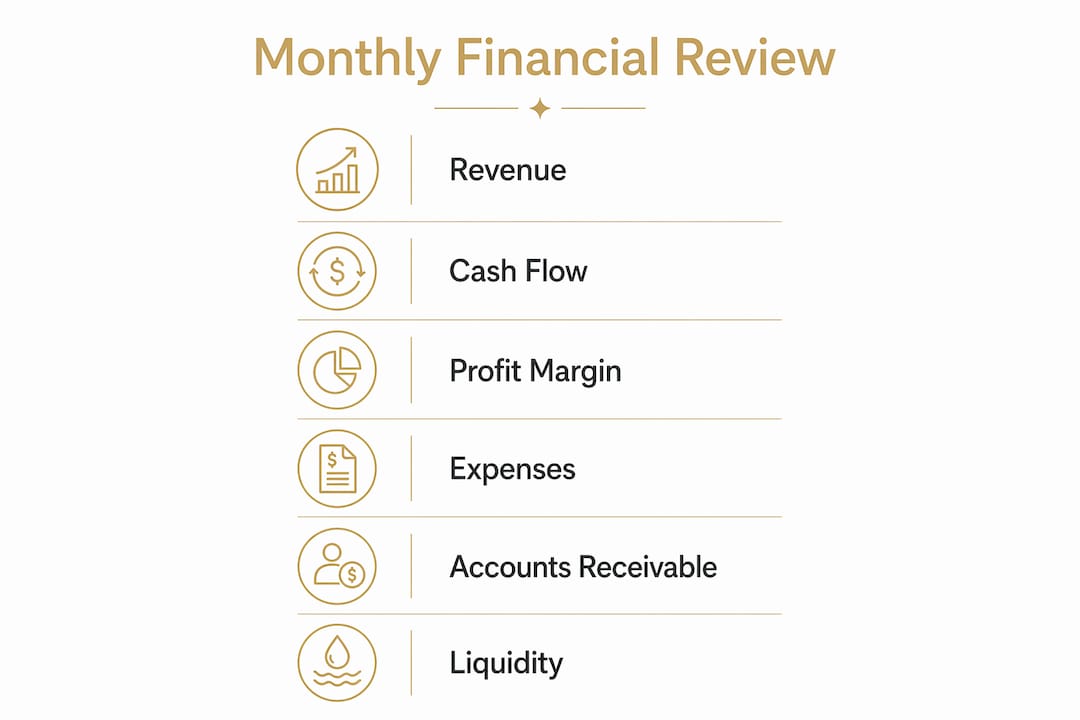

The table below covers the six key metrics every small business owner should track monthly.

| Metric | What it measures | Warning sign |

|---|---|---|

| Revenue | Total sales for the period | Declining trend over 2–3 months |

| Net margin | Profit as a percentage of revenue | Margin shrinking while revenue grows |

| Payroll as % of revenue | Labor cost relative to income | Exceeds industry norms for your sector |

| Cash balance | Actual cash on hand | Falling below one month of operating expenses |

| Accounts receivable | Money owed to you by customers | Rising total signals slow collections |

| Debt levels | Total liabilities on the balance sheet | Growing faster than assets or revenue |

Operating cash flow is a more reliable liquidity measure than net income. Net income includes non-cash items like depreciation and is subject to accounting choices. Operating cash flow cuts through that noise and shows what the business actually generated in real money.

Pro Tip: When accounts receivable keeps rising month over month, your income statement may show strong sales while your cash balance drops. That pattern signals a collections problem, not a growth success.

Step-by-step approach to reading your financials each month

A monthly review does not need to take more than 30 minutes. The goal is consistency, not perfection. Tracking six key numbers monthly converts financial data into management decisions you can act on quickly.

Follow this order every month:

-

Start with the income statement. Check total revenue first. Then look at gross profit (revenue minus cost of goods sold). Then find net income at the bottom. Ask: did we make money this period, and is the margin holding?

-

Move to the balance sheet. Confirm that assets still exceed liabilities. Check accounts receivable for any large or aging balances. Review total debt and compare it to last month. Ask: is the business financially stable right now?

-

Finish with the cash flow statement. Look at operating cash flow first. Then check the ending cash balance. Compare it to the prior month. Ask: did we generate real cash, or did profit exist only on paper?

-

Compare across periods. Pull the same reports from the prior month and the same month last year. Trends matter more than any single number. A one-month dip is noise. A three-month decline is a signal.

-

Write down one question. After reviewing all three reports, write down the one number that concerns you most. Bring it to your bookkeeper or accountant. That habit alone catches most problems before they become crises.

-

Check payroll as a percentage of revenue. Payroll is typically the largest expense for service businesses. If it creeps above your target range without a corresponding revenue increase, that is a cost structure issue to address immediately.

Pro Tip: Set a recurring calendar block on the first Monday of each month for your financial review. Treat it like a client meeting. Owners who review financials on a fixed schedule catch cash flow problems an average of 60 days earlier than those who review sporadically.

For a deeper look at how bookkeeping connects to cash flow management, the cash flow bookkeeping guide from Kelliworks covers the practical steps in detail.

Common mistakes when reading small business financial reports

Most financial reporting errors are preventable. The mistakes below account for the majority of confusion small business owners experience when reviewing their books.

-

Mixing personal and business finances. This is the most costly error in small business accounting. It distorts every line of every report and creates serious tax compliance problems. Open a dedicated business checking account and use it exclusively for business transactions from day one.

-

Ignoring the cash flow statement. Many owners focus only on the income statement because profit feels like the most important number. Profit is an accounting concept. Cash is what pays your bills. Skipping the cash flow statement means missing the most direct measure of business survival.

-

Reading reports in isolation. The income statement, balance sheet, and cash flow statement are designed to be read together. A strong income statement paired with a weak cash flow statement and rising liabilities on the balance sheet tells a very different story than any one report alone.

-

Confusing revenue with profit. Revenue is the top line. Profit is what remains after all expenses. A business can grow revenue quickly while losing money on every sale. Always trace the path from revenue to net income.

-

Relying on accounting profit for major decisions. Accounting profit includes non-cash items. Before making a large purchase, hiring decision, or loan application, check operating cash flow first. That number reflects the actual financial capacity of the business.

-

Skipping monthly reviews. Financial statements are diagnostic tools, not just documents for tax season. Reviewing them only once a year means you are reacting to problems instead of preventing them.

For guidance on avoiding common accounting pitfalls, the financial consulting vs. bookkeeping guide from Kelliworks explains when each type of professional support makes the most sense.

Key Takeaways

Reading all three financial statements together every month is the most reliable way to protect and grow a small business.

| Point | Details |

|---|---|

| Three statements, three views | The income statement, balance sheet, and cash flow statement each reveal a distinct aspect of financial health. |

| Cash flow beats profit | Operating cash flow is a more reliable measure of liquidity than net income for day-to-day decisions. |

| Six numbers monthly | Tracking revenue, net margin, payroll %, cash balance, accounts receivable, and debt catches problems early. |

| Separation of finances | Dedicated business accounts are the foundation of accurate reporting and clean tax compliance. |

| Consistency over complexity | A monthly 30-minute review done consistently outperforms an annual deep dive done once a year. |

What I have learned from years of working with small business financials

Most small business owners I work with are not afraid of numbers. They are afraid of the wrong numbers. They worry that their financials will reveal something they cannot fix. What I have found is the opposite. The owners who review their statements regularly are the ones who catch problems while they are still small. The ones who avoid their financials are the ones who get surprised.

The gap between profit and cash is the single most important relationship to understand. I have seen businesses with strong income statements and empty bank accounts. Every time, the cash flow statement told the story months before the crisis hit. If you read nothing else, read that report.

Financial literacy for entrepreneurs does not require an accounting degree. It requires a habit. Thirty minutes a month, six numbers, three reports. That is the practice. The Michigan SBDC describes financial statements as the vital signs of a business, and that framing is exactly right. You would not skip a health checkup for years and expect to catch a problem early. Your financials deserve the same attention.

The owners I see grow consistently are not the ones with the most complex financial models. They are the ones who know their numbers cold every single month. That knowledge is available to every business owner. You just have to build the habit.

— Kelli

Kelliworks is here when the numbers get complicated

Reading your own financial statements builds confidence and clarity. At some point, most small business owners benefit from a professional set of eyes on those same reports.

Kelliworks operates as a full-service virtual accounting department for small businesses. Our services cover bookkeeping, tax preparation, and financial consulting, all designed to give you accurate reports you can actually use. We help you understand what your numbers mean, identify cost-saving opportunities, and stay compliant without the stress. Whether you need a one-time review or ongoing monthly support, Kelliworks provides personalized service built around your business. Schedule a free consultation and get clarity on your financials today.

FAQ

What are the three main financial statements for small businesses?

The three primary financial statements are the income statement, the balance sheet, and the cash flow statement. Each one measures a different aspect of financial health and all three should be reviewed together.

Why is cash flow more important than profit for small businesses?

Operating cash flow reflects actual cash generated by the business, while net income includes non-cash accounting items. A business can show a profit and still fail if it runs out of cash.

How often should a small business owner review financial statements?

A monthly review is the recommended frequency. Tracking six key metrics each month, including revenue, cash balance, and accounts receivable, catches financial issues before they become serious problems.

What is the biggest mistake small business owners make with their financials?

Mixing personal and business finances is the most common and costly error. It distorts every financial report and creates tax compliance risks that are difficult and expensive to untangle.

Do I need an accountant to read my financial statements?

You do not need an accountant to read your statements, but professional support helps you interpret them accurately and act on what you find. A bookkeeper or financial consultant can flag issues you might miss and help you build better financial habits over time.

3 Responses