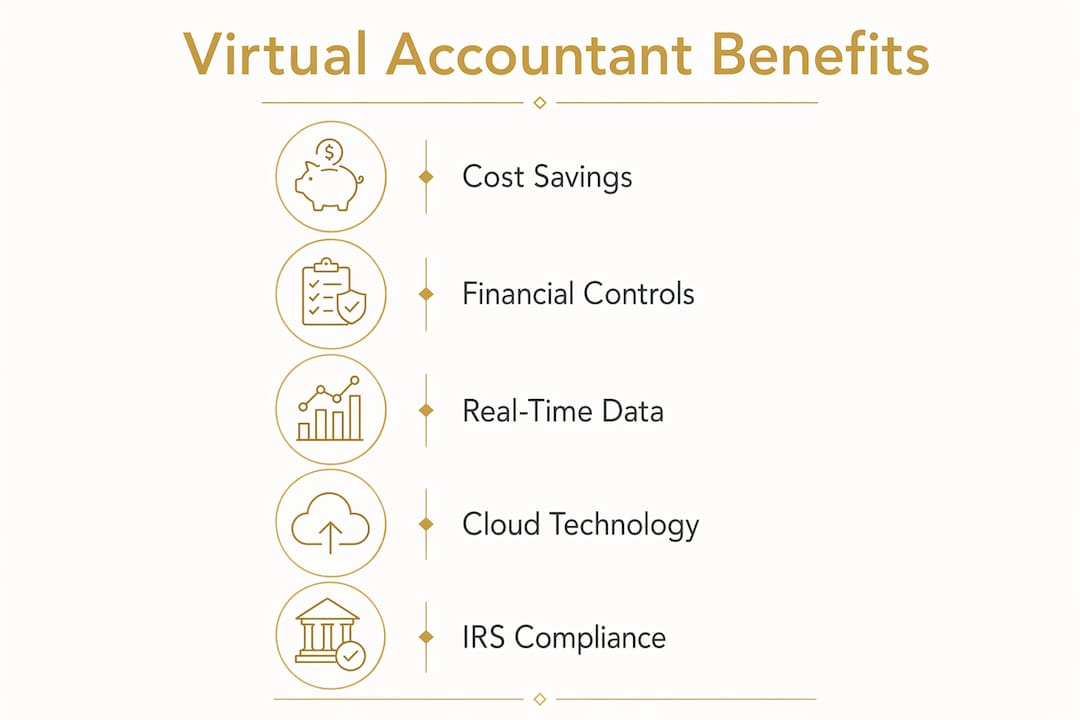

A virtual accountant is a credentialed professional who manages your business finances remotely, delivering the same expertise as an in-house hire without the overhead costs. For small business owners, this model solves two persistent problems at once: the high cost of full-time accounting staff and the stress of managing complex financial records alone. The IRS recordkeeping standards require businesses to maintain clear, organized records of income and expenses, and a virtual accountant makes that compliance achievable without consuming your time. Understanding why hire a virtual accountant comes down to three core advantages: lower costs, stronger financial controls, and real-time access to your numbers.

Why hire a virtual accountant to save money?

Hiring a virtual accountant costs significantly less than bringing on a full-time employee. A full-time in-house accountant comes with salary, payroll taxes, health insurance, retirement contributions, office space, and software licenses. A virtual accounting arrangement eliminates most of those costs because you pay only for the services you actually need.

The savings go beyond the obvious line items. When you outsource accounting tasks, you also avoid the cost of recruiting, onboarding, and training. You skip the productivity loss that comes when an in-house employee leaves. You remove the need to purchase and maintain accounting software infrastructure, since cloud accounting platforms are typically included in virtual service packages.

Here is where small business owners often leave money on the table:

- Payroll overhead: Employer-side taxes and benefits typically add 20–30% on top of base salary for any full-time hire.

- Error correction costs: Accounting mistakes caught late require professional cleanup that costs far more than prevention.

- Missed deductions: Without expert oversight, deductible expenses go unclaimed. The IRS filing requirements for small businesses vary by structure, and a virtual accountant tracks every applicable deduction.

- Software duplication: Many owners pay for accounting tools they underuse. Virtual accountants consolidate those tools into one workflow.

- Time cost: Hours you spend on bookkeeping are hours not spent on revenue-generating work.

Pro Tip: Calculate your hourly rate as a business owner, then multiply it by the hours you spend on accounting each month. That number is the true cost of doing it yourself.

The benefits of virtual bookkeeping show up most clearly in the first year, when owners realize how much time and money they were losing to financial tasks that fall outside their core skills.

What financial controls does a virtual accountant provide?

Outsourced accounting adds trained oversight that single-person bookkeeping cannot replicate. When one person handles all financial tasks with no review, errors and unauthorized expenses go undetected. Outsourced accounting acts as an internal control mechanism, catching discrepancies before they become costly problems.

The risk reduction is concrete. A virtual accountant reviews transactions regularly, flags unusual patterns, and reconciles accounts on a defined schedule. That consistent review cycle is what separates proactive financial management from reactive tax-time cleanup.

Key financial controls a virtual accountant delivers:

- Transaction review: Regular reconciliation catches duplicate charges, unauthorized expenses, and miscategorized costs.

- Fraud detection: A second set of trained eyes on your accounts reduces the risk of unnoticed internal or external fraud.

- Audit readiness: The IRS emphasizes that good records speed up audits and support every item on your tax return. A virtual accountant keeps those records current.

- Accurate financial statements: Profit and loss statements and balance sheets prepared on a regular basis give you a clear picture of business health, not just a year-end snapshot.

- Tax compliance: CPAs in outsourced firms follow strict ethical and continuing education standards, reducing your audit risk and keeping you compliant with changing tax rules.

Pro Tip: Ask your virtual accountant to deliver a brief monthly financial summary, not just a year-end report. That single habit catches cash flow problems three to six months earlier than annual reviews.

The financial consulting vs. bookkeeping distinction matters here. A strong virtual accountant does both: they keep your records clean and interpret what those records mean for your business decisions.

How does cloud accounting technology improve virtual accounting services?

Cloud accounting is the technical foundation that makes virtual accounting work. It gives both you and your accountant real-time access to the same financial data from any device with an internet connection. Cloud platforms use bank feeds and automated workflows to keep transactions current without manual data entry, which reduces errors and saves time.

The practical benefits for small business owners are direct:

- Real-time cash flow visibility: You can check your financial position any time, not just when your accountant sends a report.

- Faster decision making: When you are evaluating a new hire, a lease, or a bulk purchase, current financial data lets you decide with confidence.

- Collaborative access: Your accountant, bookkeeper, and tax preparer all work from the same data set, eliminating version conflicts and duplicate work.

- Automatic backups: Cloud platforms store your financial history securely, protecting you from data loss.

- Scalable capacity: As your business grows, cloud tools scale with you without requiring new software purchases or server upgrades.

The table below shows how cloud accounting changes the working relationship between a small business owner and a virtual accountant.

| Task | Without cloud accounting | With cloud accounting |

|---|---|---|

| Bank reconciliation | Manual, monthly, error-prone | Automated daily via bank feeds |

| Financial reporting | Delayed, often quarterly | Available in real time |

| Document sharing | Email attachments, version confusion | Centralized, always current |

| Tax preparation | Year-end scramble | Ongoing, organized throughout the year |

| Cash flow monitoring | Reactive | Proactive, with early warning signals |

Managing cash flow is where cloud accounting delivers the most immediate value. Owners who can see their cash position daily make better decisions about spending, collections, and growth investments.

When should a small business hire a virtual accountant?

The right time to hire a virtual accountant is earlier than most owners think. Many wait until tax season creates a crisis. The owners who benefit most are those who bring in virtual accounting support before complexity outpaces their ability to manage it alone.

Virtual accounting reduces operational burden and provides real-time reporting, which means the stress reduction benefit is ongoing, not just at tax time. The earlier you establish clean financial processes, the more value you extract from the relationship.

Watch for these signals that your business is ready:

- You have hired your first employee or are planning to. Payroll adds tax obligations that require accurate, timely recordkeeping.

- You carry inventory. Inventory accounting requires tracking cost of goods sold, which affects your tax liability directly.

- You sell in multiple states. Multi-state sales create sales tax obligations that vary by jurisdiction and change frequently.

- You are applying for a loan or line of credit. Lenders require organized financial statements, and good records increase your chances of securing financing.

- You spend more than five hours per month on bookkeeping. That time has a real cost, and it grows as your business does.

- You have missed a tax deadline or underpaid estimated taxes. These are signs that your current system is not keeping up.

- You are planning significant growth. A virtual accountant helps you model the financial impact of expansion before you commit.

The cost-saving accounting strategies available to small businesses multiply when you have a professional managing the numbers from the start. Waiting until problems appear means paying to fix what could have been prevented.

Key takeaways

Hiring a virtual accountant delivers measurable cost savings, stronger financial controls, and real-time data access that small business owners cannot replicate by managing finances alone.

| Point | Details |

|---|---|

| Cost savings are concrete | Virtual accounting eliminates salary overhead, benefits, and software costs tied to full-time staff. |

| Oversight reduces risk | Regular transaction review catches errors and fraud that single-person bookkeeping misses. |

| Cloud tools enable real-time decisions | Bank feeds and automated workflows give owners current financial data without manual entry. |

| Early hiring pays off | Bringing in a virtual accountant before complexity grows prevents costly cleanup and missed deductions. |

| IRS compliance is ongoing | Good records prepared year-round, not just at tax time, protect you in audits and support every deduction. |

What I have learned from working with small business owners on virtual accounting

The biggest mistake I see is owners treating virtual accounting as a once-a-year tax service. They hand over a shoebox of receipts in april and expect a miracle. That approach wastes most of the value a virtual accountant can deliver.

The owners who get the most out of this arrangement are the ones who treat their accountant as a monthly partner. They send clean, categorized transactions. They respond to questions quickly. They show up for a 30-minute monthly review call. That rhythm is what turns bookkeeping into genuine financial insight.

I have also seen owners underestimate how much recordkeeping matters beyond taxes. Clean financial records are what you show a bank when you need a loan. They are what you show a buyer if you ever sell the business. They are what protects you if the IRS asks questions. A virtual accountant builds that asset for you continuously, not just in april.

The practical advice I give every new client: set up electronic bank feeds on day one, use a dedicated business account for every transaction, and never mix personal and business expenses. Those three habits make everything else easier and cheaper.

— Kelli

Kelliworks virtual accounting services for small businesses

Small business owners who want expert financial management without the cost of in-house staff have a clear option with Kelliworks.

Kelliworks operates as a full-service virtual accounting department for small businesses and entrepreneurs. Services include bookkeeping, tax preparation, and financial consulting, all delivered remotely with the personal attention your business deserves. Every client gets a tailored approach built around their specific financial situation, not a generic package. Whether you are just starting out or managing a growing team, Kelliworks helps you stay organized, compliant, and confident in your numbers. Schedule a free consultation to see how virtual accounting can work for your business.

FAQ

What is a virtual accountant?

A virtual accountant is a credentialed accounting professional who manages your business finances remotely using cloud-based tools. They provide the same services as an in-house accountant, including bookkeeping, tax preparation, and financial reporting, without requiring a physical office presence.

How does a virtual accountant save money for small businesses?

A virtual accountant eliminates the costs of salary, benefits, office space, and software infrastructure tied to a full-time employee. You pay only for the services you need, and you avoid the expense of accounting errors caught too late.

Is virtual accounting safe and secure?

Cloud accounting platforms use encrypted bank feeds and secure document storage, making virtual accounting as safe as traditional in-house methods. Reputable virtual accountants, including CPAs, follow strict professional and ethical standards that protect your financial data.

When is the right time to hire a virtual accountant?

The right time is before complexity outpaces your ability to manage finances alone. Key triggers include hiring employees, carrying inventory, selling across multiple states, or applying for business financing.

How does a virtual accountant help with IRS compliance?

A virtual accountant maintains organized records year-round that meet IRS recordkeeping requirements, supports every deduction on your tax return, and reduces your risk in the event of an audit.

2 Responses