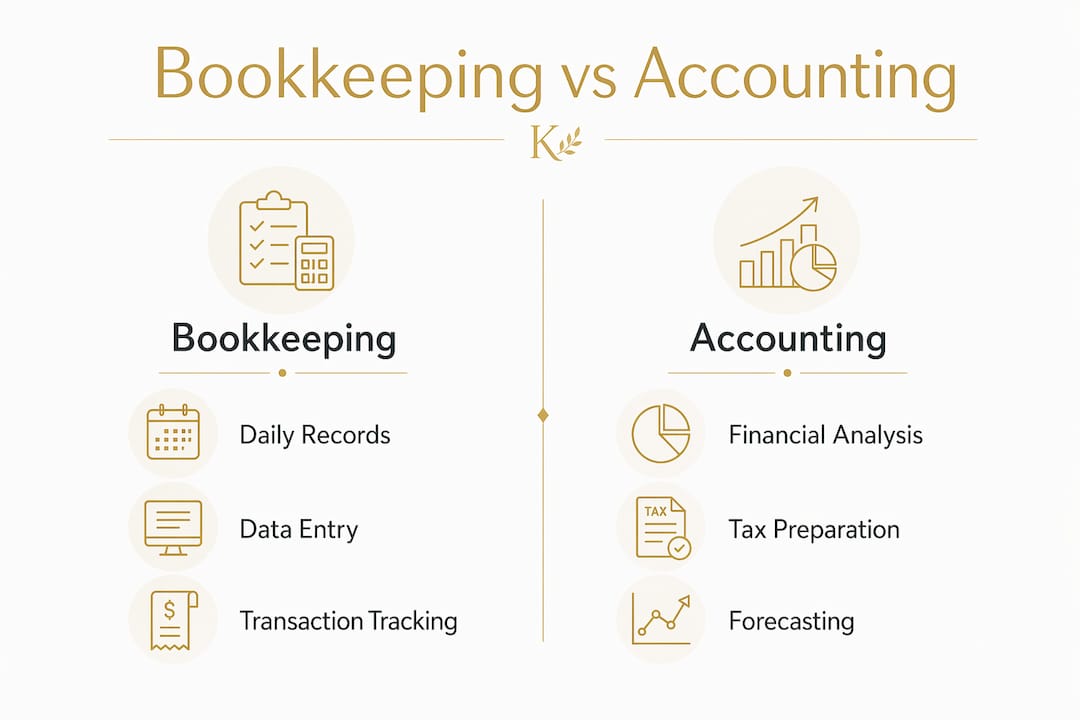

Bookkeeping is defined as the daily recording of every financial transaction your business makes, while accounting is the analysis and interpretation of those records to produce financial statements, tax strategy, and compliance reports. Both functions are distinct, and confusing them costs small business owners real money. Bookkeeping feeds the general ledger with clean, organized data. Accounting uses that data to guide decisions, satisfy IRS regulations, and plan for growth. Understanding the difference between bookkeeping and accounting is the first step toward building a financially healthy business.

What are the core functions of bookkeeping vs accounting?

Bookkeeping is the day-to-day, tactical recording of financial transactions. Accounting is the higher-level analysis that turns those records into financial statements, tax strategy, and compliance reports. The two roles are not interchangeable. They are sequential. Bookkeeping creates the foundation; accounting builds on it.

What bookkeepers actually do

Bookkeeping functions include a specific set of repeating tasks:

- Recording every sale, purchase, and payment into the general ledger

- Categorizing expenses by type (payroll, supplies, rent, software)

- Reconciling bank accounts monthly to catch errors and fraud

- Managing accounts payable and accounts receivable

- Sending and tracking invoices, and following up on late payments

A freelance graphic designer, for example, needs someone tracking every client payment, software subscription, and equipment purchase. Without that daily record, tax season becomes a guessing game.

What accountants actually do

Accountants prepare financial statements, analyze operations, and file taxes. They also handle forecasting, budgeting, and business advisory work. A Certified Public Accountant (CPA) carries professional credentials that allow them to sign off on audits and represent clients before the IRS. That credential matters when your business faces a tax audit or needs a formal financial review for a loan application.

Accounting without clean bookkeeping is nearly impossible. An accountant who receives disorganized records spends billable hours cleaning data instead of delivering strategy. That is why the two roles work best together.

How do bookkeeping and accounting affect your financial health?

Bookkeeping keeps your business compliant and organized day to day. Accounting turns that organization into growth decisions. Both affect your financial health, but in different ways and on different timelines.

Here is how each role contributes in practice:

- Preventing costly errors. Accurate bookkeeping catches duplicate charges, missed payments, and bank discrepancies before they compound. A single unreconciled account can distort your profit and loss statement for an entire quarter.

- Supporting tax compliance. Clean records mean your accountant files accurate returns and identifies every deduction you qualify for. Poor bookkeeping leads to missed deductions and potential IRS penalties.

- Enabling strategic planning. Accountants use your financial statements to project cash flow, advise on pricing, and identify whether your business can afford to hire or expand.

- Preparing for audits. If the IRS audits your business, organized bookkeeping records are your primary defense. Accountants use those records to respond to inquiries and protect your position.

- Managing cash flow velocity. Viewing your revenue cycle as an integrated billing system, not just a compliance task, gives you control over when money comes in and goes out.

Pro Tip: Keep your books updated weekly, not monthly. Weekly reconciliation takes 30 minutes and prevents the hours-long scramble that happens when you wait until month end.

The synergy between the two roles is where real financial health lives. Businesses that invest in both functions consistently make better decisions and carry less financial risk than those that treat bookkeeping as optional.

What qualifications and tools separate bookkeepers from accountants?

The credentials, skills, and software each role uses are meaningfully different. Knowing those differences helps you hire the right person and set the right expectations.

Credentials and training

Bookkeepers typically hold a certificate or associate degree in accounting or business. Some earn certification through the American Institute of Professional Bookkeepers (AIPB). Certified Public Accountants (CPAs) hold bachelor’s degrees and pass a rigorous four-part exam administered by state boards. CPAs bear legal responsibility for tax filings and audits. That accountability is why their hourly rates reflect a different level of risk and expertise.

Skills that define each role

The skill sets are genuinely different, not just different in degree:

- Bookkeepers excel at precision data entry, attention to detail, and consistency. Their value comes from accuracy and reliability, not financial interpretation.

- Accountants apply analytical thinking, financial modeling, and regulatory knowledge. They read patterns in your numbers and translate them into advice you can act on.

- Both roles benefit from proficiency in accounting software, which now automates much of the manual data entry that once defined bookkeeping work.

How software is reshaping both roles

Accounting software automates many tasks, shifting bookkeepers from manual data entry toward oversight and exception handling. Accountants benefit because they receive cleaner data faster, which frees them to focus on forecasting and advising rather than correcting errors. Billing software handles invoicing and payment tracking, while full accounting platforms manage the broader general ledger, including profit and loss reporting and compliance. Integrated platforms automate the path from invoice to ledger entry, reducing the manual steps between the two roles.

Pro Tip: If you are a freelancer or solo business owner, start with accounting software that includes invoicing. You get basic bookkeeping functions built in, and you can add a bookkeeper or accountant as your revenue grows.

When should you hire a bookkeeper, an accountant, or both?

The decision depends on your business size, complexity, and how much time you currently spend on financial tasks. Most small business owners wait too long to get help, and that delay costs more than the professional fees would have.

Signs you need a bookkeeper

- You spend more than 5 hours weekly on financial organization, data entry, or chasing invoices

- Your invoicing and accounts receivable are inconsistent or behind

- You want clean monthly reports but do not have time to produce them

- You are mixing personal and business expenses without a clear system

Signs you need an accountant

- Your tax filing involves multiple income streams, depreciation, or business deductions

- Your annual revenue exceeds $500,000

- You are planning to hire employees, take on investors, or apply for a business loan

- You need financial forecasting to support a major business decision

The case for hiring both

Bookkeepers charge $20–$50 per hour for data entry and basic reporting. Accountants charge $150–$400 per hour for strategic advice and compliance services. Hiring both is not redundant. It is efficient. Your bookkeeper keeps the records current and accurate. Your accountant uses those records to minimize your tax liability and guide your growth. Together, they cost less than the penalties, missed deductions, and poor decisions that come from managing finances without professional support.

A virtual accounting model, like the one Kelliworks offers, combines both functions under one roof. That structure gives small business owners and freelancers access to bookkeeping best practices and CPA-level accounting without the overhead of hiring two separate professionals. For businesses navigating compliance requirements, a structured approach to financial and tax obligations also reduces the risk of costly oversights.

What I have learned from working with small business finances

After years of working with small business owners and freelancers, the pattern I see most often is this: business owners underinvest in bookkeeping and then overpay for accounting cleanup. Messy records do not just slow things down. They cost real money in accountant hours spent untangling transactions instead of planning strategy.

The second mistake I see is treating bookkeeping and accounting as the same job. Owners hand everything to one person and expect both daily transaction management and high-level tax strategy. That rarely works well. The skills are different. The time requirements are different. Expecting one generalist to do both usually means neither gets done properly.

What actually works is clean, weekly bookkeeping paired with quarterly accountant reviews. That rhythm keeps your records current, catches problems early, and gives your accountant the organized data they need to deliver real financial insight. Technology helps, but it does not replace the judgment that comes from a professional who knows your business.

The business owners I have seen grow fastest are the ones who stop treating their finances as a burden and start treating them as a management tool. Your books tell you where your money is going, where your profit is hiding, and where your next opportunity is. You just need the right people reading them.

— Kelli

Kelliworks financial services for small business owners

Small business owners and freelancers deserve financial support that goes beyond basic tax filing. Kelliworks operates as a full-service virtual accounting department, handling bookkeeping, tax preparation, and financial consulting in one place.

Whether you need organized monthly books, a CPA to handle your tax strategy, or both, Kelliworks builds a plan around your business. Clients consistently report less stress, better financial clarity, and more confidence in their decisions after working with the Kelliworks team. If you are ready to stop managing your finances alone, hiring a virtual accountant is a practical, cost-effective first step. You can also explore cost-saving accounting strategies tailored specifically to small businesses.

Key takeaways

Bookkeeping records your financial transactions daily, and accounting analyzes those records to produce the tax strategy, financial statements, and business insights that drive growth.

| Point | Details |

|---|---|

| Bookkeeping is foundational | Clean, daily transaction records make every accounting function faster and more accurate. |

| Accounting delivers strategy | CPAs use your books to minimize taxes, forecast cash flow, and guide business decisions. |

| Hire based on your workload | Spend over 5 hours weekly on finances? Start with a bookkeeper. Revenue over $500,000? Add an accountant. |

| Rates reflect different value | Bookkeepers charge $20–$50 per hour; accountants charge $150–$400 per hour for strategic work. |

| Virtual services combine both | A virtual accounting firm gives you bookkeeping and CPA-level accounting without two separate hires. |

FAQ

What is the main difference between bookkeeping and accounting?

Bookkeeping is the daily recording of financial transactions into the general ledger. Accounting is the analysis of those records to produce financial statements, tax filings, and business strategy.

Does a bookkeeper need a CPA license?

No. Bookkeepers typically hold a certificate or associate degree and do not require CPA certification. CPAs hold bachelor’s degrees and pass state-administered exams that authorize them to sign tax filings and conduct audits.

Can accounting software replace a bookkeeper or accountant?

Accounting software automates data entry and basic reporting, but it does not replace professional judgment. A bookkeeper provides oversight and accuracy; an accountant provides interpretation and strategy that software cannot replicate.

When does a freelancer need an accountant instead of a bookkeeper?

A freelancer needs an accountant when their tax situation involves multiple income streams, self-employment deductions, quarterly estimated taxes, or business growth planning that requires financial forecasting.

What does invoicing have to do with bookkeeping?

Invoicing is a single payment request, while billing is a full operational system that includes quoting, collections, and reconciliation. Accurate invoicing feeds directly into your bookkeeping records and affects your accounts receivable balance and cash flow reporting.