Small business bookkeeping is the systematic process of recording every financial transaction your company makes, from sales and expenses to payroll and loan payments. The industry term is “bookkeeping,” and it forms the foundation of all small business accounting. Without accurate records, tax preparation becomes guesswork, cash flow analysis loses meaning, and lenders have nothing to evaluate. Tax authorities require businesses to retain supporting financial documents for at least 6 years after the last related tax year. That requirement alone signals how seriously regulators treat financial record-keeping, and how seriously you should too.

What is small business bookkeeping and why does it matter?

Bookkeeping is the daily or weekly process of recording financial transactions. Accounting, by contrast, involves analyzing and interpreting those records to prepare financial statements and guide business decisions. The two disciplines work together, but they are not the same thing. Bookkeeping comes first. Without it, accounting has nothing to work with.

The importance of bookkeeping goes beyond compliance. Clean, current records tell you whether your business is profitable, which clients pay late, and where your money actually goes each month. Business owners who skip regular bookkeeping often discover problems only at tax time, when fixing them costs far more in time and professional fees than prevention would have.

Bookkeeping forms the backbone of accounting, and clean records drastically reduce tax preparation costs and errors. That connection is direct and measurable. A business with organized monthly records spends a fraction of the time in tax preparation compared to one that hands over a shoebox of receipts in april.

What are the main bookkeeping methods and how do they differ?

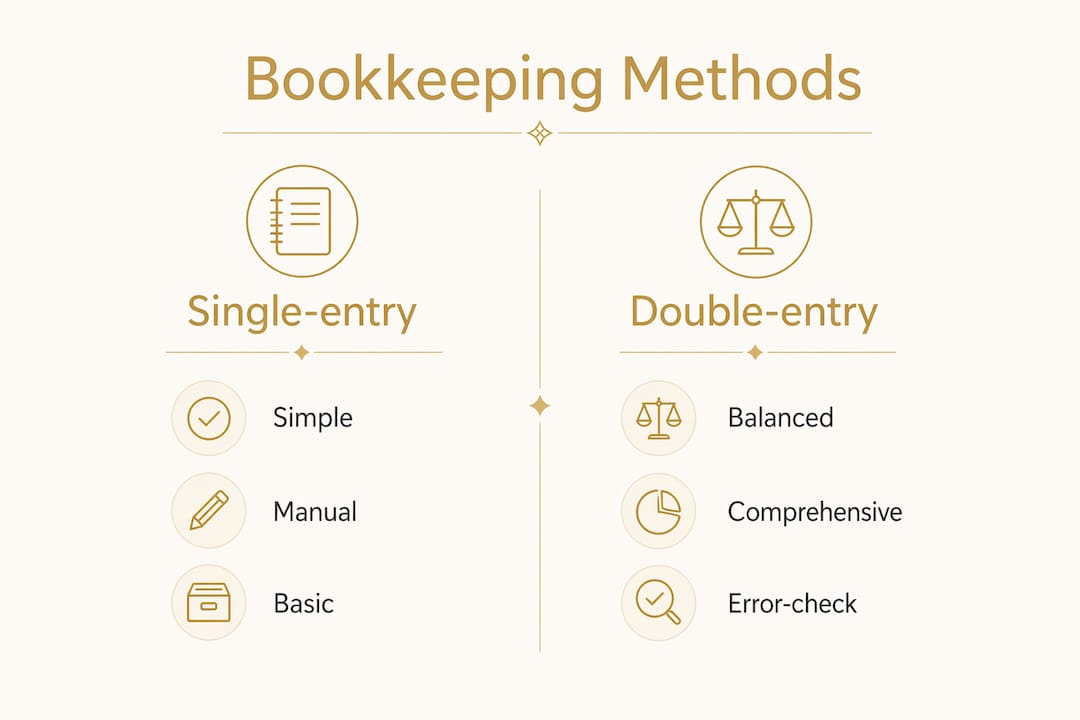

Two primary methods exist for recording business transactions: single-entry and double-entry bookkeeping. Choosing the right one depends on your transaction volume and how much financial detail you need.

Single-entry bookkeeping

Single-entry bookkeeping records each transaction once, similar to how you track entries in a personal checkbook. It works for very small businesses with minimal transactions, but it offers no built-in error detection and gives you an incomplete financial picture. If a number is entered wrong, nothing in the system flags it.

Double-entry bookkeeping

Double-entry bookkeeping records every transaction twice, as both a debit and a credit. This keeps accounts balanced and makes errors visible. It is the standard method for any business that needs accurate financial reporting, applies for loans, or plans to grow. The general ledger sits at the center of this system, organizing every transaction by account category.

Cash basis vs. accrual accounting

These two accounting bases affect when you record transactions. Cash basis records income when received and expenses when paid. Accrual basis records income when earned and expenses when incurred, regardless of when cash moves. Most small businesses start on cash basis for its simplicity, but accrual accounting gives a more accurate picture of financial health over time.

| Method | How it works | Best for | Error detection |

|---|---|---|---|

| Single-entry | One entry per transaction | Sole proprietors, minimal volume | None built in |

| Double-entry | Debit and credit per transaction | Most small businesses | Yes, built in |

| Cash basis | Record when cash moves | Simple operations | N/A |

| Accrual basis | Record when earned or incurred | Growing businesses | N/A |

A chart of accounts is the organized list of every account your business uses, such as revenue, rent, payroll, and supplies. It gives your bookkeeping system structure and makes financial reports consistent and readable.

What are the best practices for setting up your bookkeeping system?

Setting up a solid bookkeeping system from the start saves you from expensive corrections later. The following practices are the foundation of reliable small business financial management.

- Open a dedicated business bank account. Mixing personal and business finances is the most common and costly mistake small business owners make. A separate account creates a clean transaction record and protects you from liability and tax complications.

- Organize and retain all financial documents. Keep receipts, invoices, bank statements, and payroll records. Digital copies count, but you must retain them for at least 6 years to meet tax authority requirements.

- Set a consistent bookkeeping schedule. Weekly is better than monthly. A short session each week keeps records current and prevents the backlog that turns into a multi-day cleanup before tax season.

- Reconcile your bank statements monthly. Reconciliation means matching your recorded transactions against your actual bank statement. It catches errors, duplicate entries, and unauthorized charges before they compound.

- Use a chart of accounts from day one. Categorizing transactions consistently from the beginning makes financial reports meaningful and tax preparation straightforward.

Pro Tip: Weekly bookkeeping of just 15–30 minutes prevents the costly catch-up sessions that can consume 20 or more hours before a tax deadline. Block it on your calendar like any other business appointment.

Tracking cash flow with bookkeeping is one of the most practical benefits of staying current. When your records are up to date, you can see exactly how much cash you have, what is owed to you, and what bills are coming due. That visibility is what separates businesses that plan ahead from those that react to crises.

Pro Tip: Set up a simple digital folder system organized by month and document type. Scan receipts immediately using your phone. The five seconds it takes at the moment of purchase saves hours of searching later.

How can small business owners use bookkeeping software effectively?

Bookkeeping software automates the most repetitive parts of financial record-keeping. Accounting software pricing ranges from free entry-level plans up to $275 per month, depending on features, user access, and reporting depth. That range reflects a wide spectrum of capability, from basic income and expense tracking to full payroll processing and multi-user access.

When selecting software, evaluate it against these criteria:

- Transaction volume capacity. Entry-level tools handle low monthly transaction counts. As your business grows, you need software that scales without requiring a full migration.

- Automation features. Good software learns vendor classifications and auto-categorizes recurring transactions. This saves time but requires oversight.

- Bank feed integration. Direct connection to your business bank account pulls transactions automatically, reducing manual entry errors.

- Reporting quality. Profit and loss statements, balance sheets, and cash flow reports should be easy to generate and read.

- Customer support. When something goes wrong at tax time, accessible support matters. Check whether the plan you choose includes live help or limits you to community forums.

- Scalability. Choose software that can grow with you. Switching platforms mid-year is disruptive and risks data loss.

| Software tier | Typical monthly cost | Key features |

|---|---|---|

| Entry-level | Free to $20 | Income/expense tracking, invoicing |

| Mid-range | $20 to $80 | Bank feeds, payroll, basic reporting |

| Advanced | $80 to $275 | Multi-user, advanced reports, integrations |

Automated categorization learns vendor classifications but requires regular manual review to avoid accumulating errors. This is the most overlooked risk in software-based bookkeeping. A single misclassified vendor, repeated across 12 months of transactions, can distort your profit and loss statement significantly. Review categorized transactions at least monthly, not just at year end.

For guidance on cost-effective bookkeeping options that fit different budget levels, Kelliworks has published a current resource covering software and service strategies for 2026.

When should you consult a professional accountant?

Bookkeeping and accounting serve different purposes, and knowing when to bring in a professional saves money and prevents costly mistakes. Bookkeeping is the recording function. Accounting is the analysis and strategy function built on top of those records.

Small business owners should consult a professional accountant at least every few months, even when managing their own books. Quarterly reviews catch misclassifications, identify tax deductions you may have missed, and confirm that your records meet compliance standards. A CPA reviewing clean, organized books spends far less time, and charges far less, than one untangling a year of disorganized records.

Clean bookkeeping directly reduces your tax preparation bill. When a tax professional receives organized, categorized records, they can focus on strategy and deductions rather than data entry and error correction. The difference between bookkeeping and financial consulting is worth understanding clearly, because each serves a distinct role in your financial management.

Professional guidance also supports growth. A CPA can identify when your business structure should change, when you need to adjust estimated tax payments, or when a financial decision carries unexpected tax consequences. DIY bookkeeping and professional accounting work best as a team, not as substitutes for each other.

Pro Tip: Before each quarterly accountant meeting, prepare a one-page summary of major financial changes: new vendors, large purchases, new revenue streams, or any transactions you were unsure how to categorize. This makes the review faster and more productive.

Key takeaways

Accurate, consistent bookkeeping is the single most important financial habit a small business owner can build, because it supports every other financial decision the business makes.

| Point | Details |

|---|---|

| Bookkeeping vs. accounting | Bookkeeping records transactions; accounting analyzes them. Both are necessary. |

| Document retention | Retain all financial records for at least 6 years to meet tax authority requirements. |

| Separate bank accounts | A dedicated business account prevents the most common and costly bookkeeping mistake. |

| Weekly scheduling | Fifteen to thirty minutes per week prevents 20-plus hours of catch-up at tax time. |

| Software oversight | Automated categorization requires monthly manual review to prevent compounding errors. |

What I’ve learned after years of working with small business books

Most small business owners treat bookkeeping as something to catch up on, not something to stay current with. That mindset is where the real cost hides. I have seen businesses pay three times more in tax preparation fees simply because their records were disorganized. The accountant’s time goes to sorting and correcting, not to finding deductions.

The other pattern I see consistently is underestimating how short good bookkeeping actually takes. Owners assume it requires hours they do not have. In practice, a well-organized system with a weekly 20-minute session keeps everything current. The time investment is small. The payoff at tax time, and in the clarity you gain about your own business, is significant.

My honest view is that bookkeeping is not a burden. It is the clearest window into how your business actually performs. Owners who treat it as a non-negotiable weekly task make better decisions, respond faster to problems, and feel more confident in every financial conversation, whether with a lender, a partner, or a tax professional. Combining that discipline with periodic professional review through a service like Kelliworks is the most reliable path to financial health for a small business.

— Kelli

How Kelliworks supports your bookkeeping and accounting needs

Running a business leaves little time for financial administration, and that is exactly where Kelliworks steps in. As a full-service virtual accounting department built specifically for small businesses, Kelliworks offers bookkeeping, tax preparation, and financial consulting tailored to your situation.

Whether you want to hand off your books entirely or get expert support alongside your own efforts, Kelliworks provides personalized service without the overhead of a traditional accounting firm. Explore virtual accounting services designed for small business owners, or review accounting service options to find the right level of support. For a personal conversation about your specific needs, schedule a free consultation with the Kelliworks team.

FAQ

What is the difference between bookkeeping and accounting?

Bookkeeping is the process of recording financial transactions. Accounting uses those records to analyze performance, prepare financial statements, and guide business decisions.

How long do I need to keep business financial records?

Tax authorities require businesses to retain supporting financial documents for at least 6 years after the last related tax year, including digital records.

What bookkeeping method is best for a small business?

Double-entry bookkeeping is the standard for most small businesses because it detects errors and supports full financial reporting. Single-entry works only for very low-volume operations.

How often should I review my bookkeeping software’s categorizations?

Review automated transaction categorizations at least monthly. Software learns vendor classifications but can accumulate significant errors without regular manual oversight.

When should a small business owner hire a professional accountant?

Professional accountant consultation is recommended at least every few months, even for owners who manage their own books, to catch errors and identify tax deductions.