A virtual accounting department is defined as a fully managed, remote team of accounting professionals who handle all core finance functions online using cloud-based technology. This model gives small business owners access to a staff accountant, controller, and fractional CFO without the cost or complexity of hiring in-house. The result is a complete finance function at a fraction of traditional overhead. If you have been wondering whether a virtual finance team could work for your business, this guide covers how it works, what it costs, and how to make the switch successfully.

What does a virtual accounting department explained actually mean?

A virtual accounting department is not simply a remote freelancer handling your books. It is a structured, managed team that replicates every function of an internal accounting department, delivered entirely through cloud platforms and standardized workflows.

The industry term for this model is “outsourced accounting” or “full-service outsourced accounting.” The virtual accounting department label describes the same concept from the client’s perspective. Both terms refer to the same tiered team structure covering daily transactions, financial oversight, and strategic planning.

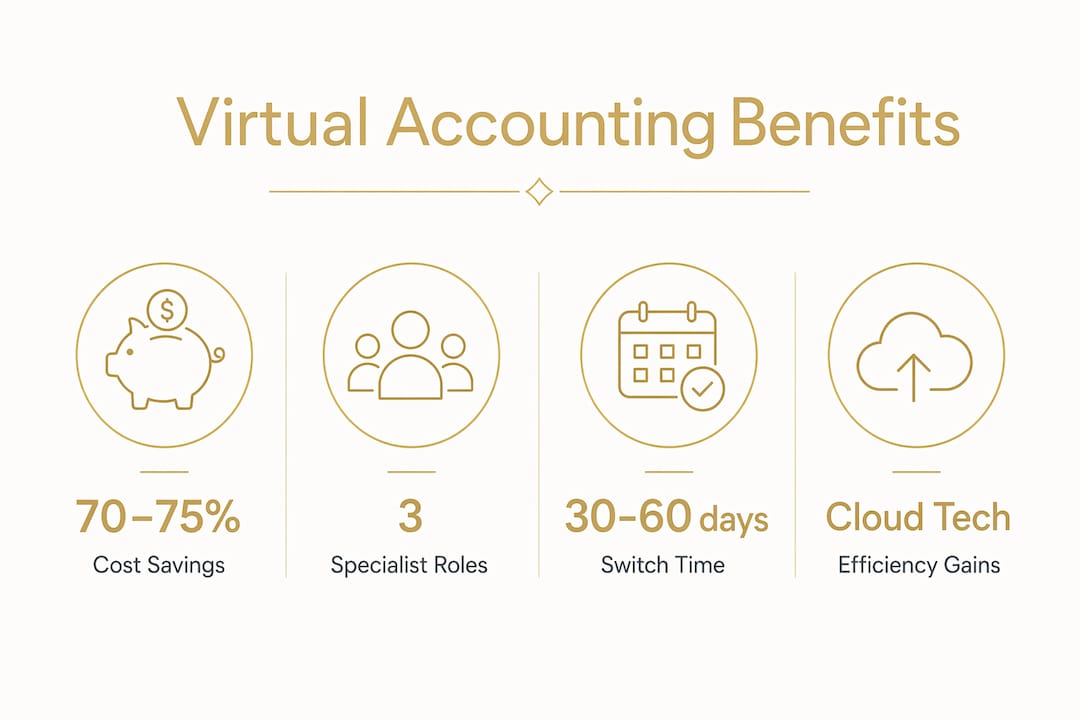

Full-service outsourced accounting divides work among three specialist roles. The staff accountant manages daily bookkeeping and transaction entry. The controller handles month-end close, reconciliations, and compliance. The fractional CFO provides financial strategy, forecasting, and advisory support. This division creates checks and balances that a single in-house hire cannot replicate.

The “virtual” part refers to cloud-enabled workflows, not just physical distance. Technology-enabled workflows unify payroll, tax tracking, and financial reporting into one connected system. That integration is what makes the model reliable, not the fact that your accountant works from another location.

What services does a virtual accounting department provide?

A virtual finance team covers the full range of accounting functions your business needs to stay compliant, organized, and financially healthy. The scope goes well beyond basic bookkeeping.

Core services typically include:

- Daily bookkeeping and transaction categorization

- Bank and credit card reconciliations

- Accounts payable and accounts receivable management

- Payroll processing and payroll tax filings

- Sales tax tracking and remittance

- Month-end close and financial statement preparation

- Annual tax preparation and planning

- Budgeting, forecasting, and cash flow analysis

- Fractional CFO advisory for growth decisions

What separates a managed team from a lone freelancer:

- A managed team includes a lead accountant, a reviewing controller, and a fractional CFO layer. Each person checks the work of the person below them.

- Managed teams provide continuity through supervisors and backup staff, so your financial history stays intact if one person leaves.

- A solo freelancer carries all institutional knowledge alone. If they leave, you start over.

Virtual accounting teams deliver financial statements and reconciliations on a structured monthly schedule, reviewed by senior staff before delivery. That review layer is the quality control most small businesses never get from a single bookkeeper.

Small businesses also benefit from embedded fraud prevention. Segregation of duties is built into the team structure, meaning no single person can both record and approve transactions. This control reduces the risk of internal fraud, which disproportionately affects small businesses.

How do virtual accounting departments save money and improve efficiency?

Cost savings are the most immediate reason small business owners switch to a virtual accounting department. The numbers are significant.

Managed virtual accounting departments cost approximately 70–75% less than equivalent in-house teams when you account for salaries, benefits, payroll taxes, and office overhead. For a small business that would otherwise need a bookkeeper, controller, and part-time CFO, that gap represents tens of thousands of dollars per year.

Pro Tip: Before comparing costs, calculate the true fully loaded cost of an in-house hire: base salary, employer payroll taxes, health insurance, paid time off, and any software or equipment you would need to provide. The real number is almost always higher than the salary alone.

Efficiency gains come from automation and standardized processes. Cloud platforms reduce manual data entry and the human errors that come with it. Month-end close cycles that once took two weeks can be completed in days when workflows are properly structured. That speed gives you financial statements you can actually use to make decisions, not reports that arrive six weeks after the period ends.

Scalability is another practical advantage. Businesses can scale their virtual accounting service levels or add team members within 5–10 business days to meet changing needs. If you land a large contract or open a second location, your accounting support grows with you. You do not need to post a job listing, conduct interviews, or wait months for a new hire to get up to speed.

Administrative burden also drops significantly. You no longer manage HR paperwork, handle accounting staff performance reviews, or worry about coverage during vacations and sick days. The provider handles all of that internally. For small business owners who wear multiple hats, that relief is real and immediate. Exploring cost-saving accounting strategies alongside a virtual team can compound these financial benefits further.

What technology and security standards power virtual accounting?

The technology infrastructure behind a virtual accounting department is what separates a reliable provider from a risky one. Cloud platforms and security controls are not optional extras. They are the foundation.

Most virtual accounting teams work inside platforms like QuickBooks Online, Xero, or NetSuite, depending on the complexity of your business. These tools connect your bank accounts, payroll system, and expense tracking into one real-time view. Your financial data is always current, and your team can access it without waiting for you to send files.

| Security standard | What it means for your business |

|---|---|

| SOC 2 Type II alignment | Provider controls are independently audited for data security and availability |

| ISO 27001 certification | Information security management meets international standards |

| Encrypted data access | Financial data is protected in transit and at rest |

| Secured workstations | Staff work on managed devices, not personal home computers |

| Monitored access controls | Only authorized team members can view your financial records |

SOC 2 Type II-aligned controls are the industry standard for virtual accounting security. A provider that cannot confirm SOC 2 alignment is a provider worth avoiding. Ask directly before signing any agreement.

Effective virtual accounting requires staff to work on secure, centrally managed workstations with encrypted access, not personal home computers. This distinction matters because personal devices are far more vulnerable to malware, phishing, and unauthorized access. A reputable provider enforces this policy across their entire team.

Pro Tip: Ask any virtual accounting provider to describe their data security policy in writing. A provider confident in their controls will answer without hesitation. Vague answers are a warning sign.

Understanding remote work productivity tools can also help you evaluate whether a virtual provider’s communication and reporting setup will fit your workflow.

How do you switch to a virtual accounting department successfully?

Transitioning to a virtual accounting model is straightforward when you plan it in advance. The most common mistakes come from rushing the process or choosing the wrong type of provider.

Steps to a successful transition:

- Assess your current state. Identify which accounting functions you handle in-house, which you outsource, and where the gaps are. Know your current software, your payroll provider, and your tax filing history.

- Define your service scope. Decide whether you need bookkeeping only, a full controller function, or fractional CFO support as well. Your revenue, transaction volume, and growth plans will guide this decision.

- Choose a managed provider over a solo freelancer. A managed team gives you continuity, oversight, and built-in quality control. A solo freelancer carries all risk on one person.

- Confirm software compatibility. Your new provider should work inside your existing platforms or help you migrate to a better one. Data migration should be planned carefully to avoid gaps in your financial history.

- Establish a service level agreement. Agree on deliverable deadlines, communication frequency, and escalation procedures before work begins. Monthly financial statements, quarterly reviews, and a defined response time for questions are standard expectations.

- Plan for onboarding time. Give your new team 30–60 days to learn your business, clean up any historical records, and establish their workflow. Do not expect perfection in week one.

A key factor many business owners overlook is understanding virtual accountant roles before selecting a provider. Knowing the difference between what a staff accountant, controller, and fractional CFO each do helps you ask better questions and choose the right service tier.

If you are currently using a mix of a part-time bookkeeper and a once-a-year tax preparer, you are already spending money on fragmented accounting support. A virtual accounting department consolidates those functions into one coordinated team, which typically costs less and produces better results.

Key Takeaways

A virtual accounting department delivers the full function of an in-house finance team at 70–75% lower cost, with built-in security controls, scalable staffing, and fraud prevention through segregation of duties.

| Point | Details |

|---|---|

| Defined service scope | Virtual accounting covers bookkeeping, payroll, tax, compliance, and fractional CFO advisory. |

| Significant cost savings | Managed teams cost 70–75% less than equivalent in-house hires when all overhead is included. |

| Built-in fraud prevention | Segregation of duties across the team structure reduces internal fraud risk for small businesses. |

| Security standards matter | SOC 2 Type II alignment and encrypted workstations are the baseline for a trustworthy provider. |

| Scalability on demand | Service levels and team size can be adjusted within 5–10 business days as your business changes. |

What I have learned from watching small businesses manage their finances

The conversation about virtual accounting almost always starts with cost. Business owners want to know if it is cheaper. It is. But the cost question misses what I think is the more important issue: continuity risk.

Most small businesses I have worked with rely on one person for their financial records. That person knows the chart of accounts, the vendor relationships, the payroll quirks, and the tax history. When that person leaves, and eventually they always do, the business loses all of that institutional knowledge overnight. A managed virtual accounting team eliminates that single point of failure. The lead accountant is supported by a supervisor and a backup. Your financial history stays intact regardless of staff changes.

The second thing I have observed is that fractional CFO access changes how business owners make decisions. When you have a controller reviewing your books and a CFO-level advisor interpreting your numbers, you stop making financial decisions based on your bank balance. You start making them based on cash flow projections, margin analysis, and actual financial goals. That shift is where real growth happens.

My advice when evaluating providers: prioritize industry experience and communication standards over price alone. A provider who knows your industry will catch issues a generalist misses. And a provider with clear reporting cadences and defined response times will feel like a true partner, not a vendor you have to chase.

— Kelli

How Kelliworks supports your virtual accounting needs

Kelliworks is a full-service virtual accounting department built specifically for small business owners who want expert financial management without the overhead of an in-house team.

Kelliworks covers the complete accounting function: staff accountant services for daily bookkeeping, controller-level oversight for month-end close and compliance, and fractional CFO advisory for financial planning and growth strategy. Every client receives personalized service, not a one-size-fits-all package. Security, accuracy, and clear communication are built into every engagement. If you are ready to see what a dedicated virtual finance team can do for your business, learn why small businesses hire virtual accountants or explore the full range of Kelliworks accounting services to find the right fit.

FAQ

What is a virtual accounting department?

A virtual accounting department is a managed, remote team of accounting professionals who handle bookkeeping, payroll, tax compliance, financial reporting, and strategic advisory for a business using cloud-based platforms.

How much does a virtual accounting department cost compared to in-house staff?

Managed virtual accounting teams cost approximately 70–75% less than equivalent in-house teams when salaries, benefits, and office overhead are included.

Is my financial data secure with a virtual accounting provider?

Reputable providers operate under SOC 2 Type II-aligned controls, use encrypted data access, and require staff to work on secured, centrally managed workstations rather than personal devices.

How long does it take to switch to a virtual accounting department?

Most businesses complete the transition within 30–60 days, including data migration and onboarding. Service levels can be scaled up or down within 5–10 business days as your needs change.

What is the difference between a virtual accountant and a virtual accounting department?

A virtual accountant is typically a single remote professional, while a virtual accounting department is a structured team with a staff accountant, controller, and fractional CFO providing layered oversight and continuity.

One Response