A financial gap is the measurable distance between where your business stands financially and where it needs to be. Identifying financial gaps in business is the first step toward closing them, and most small business owners discover these gaps far later than they should. The good news is that you do not need a finance degree to spot financial weaknesses. You need the right metrics, a consistent review process, and the discipline to look at your numbers honestly. This guide walks you through exactly that.

What financial metrics reveal gaps in your business

The three core financial statements are your starting point: the balance sheet, the income statement, and the cash flow statement. Financial statement analysis helps you evaluate liquidity, solvency, profitability, and risk by interpreting data across all three documents. Reading only one of them gives you an incomplete picture.

The metrics that matter most when you assess business finances are:

- Current ratio (current assets divided by current liabilities): a ratio below 1.0 signals you may not cover short-term obligations

- Gross margin: revenue minus cost of goods sold, expressed as a percentage; a shrinking gross margin means your core business is becoming less profitable

- Operating margin: gross profit minus operating expenses; this reveals whether your overhead is eating your earnings

- Net margin: the bottom line after all expenses and taxes

- Debt-to-equity ratio: how much of your business is financed by debt versus owner equity

- Accounts receivable aging: how long customers take to pay you, broken into 30, 60, and 90-plus day buckets

One quarter of data is not enough. Trend analysis over 8–12 quarters is more reliable than a single-period review because it filters out seasonality and one-time events. A single strong quarter can mask three weak ones.

Cash runway is another metric that often goes untracked. Cash runway tells you how many months your business can operate at its current burn rate before running out of money. A business can show a profit on paper and still run dry. Accrual accounting can mask working capital issues, which is exactly why reviewing your income statement and cash flow statement together is not optional.

Pro Tip: Benchmark your ratios against industry averages, not just your own history. A gross margin that looks stable may still be well below what healthy businesses in your sector achieve.

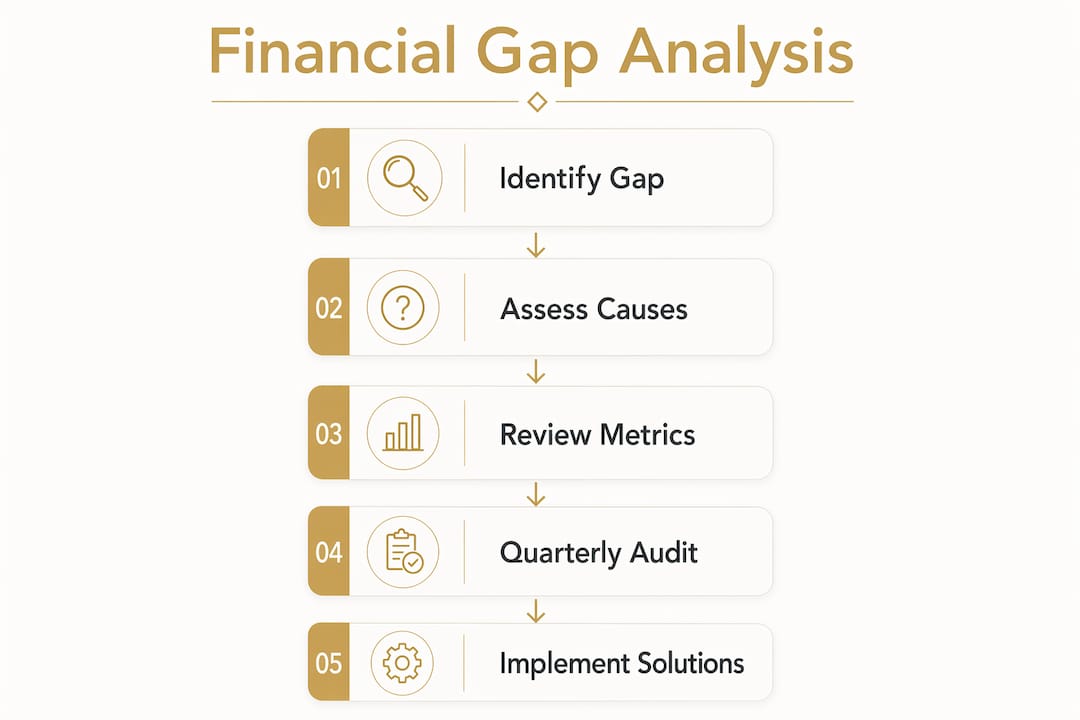

How to conduct a gap analysis on your finances

A financial gap analysis is the formal process of comparing your current financial performance against your stated goals. Here is how to do it in four steps.

-

Define your current state. Pull your last 8–12 quarters of financial statements. Calculate the key metrics listed above. Note trends, not just snapshots. Your current state is a pattern, not a single number.

-

Set clear, measurable financial goals. Vague goals like “improve cash flow” do not work. Specific goals do: “Reach a current ratio of 1.5 by december 31” or “Grow gross margin from 38% to 45% within 12 months.” Goals must be tied to your business model and growth stage.

-

Identify the gaps. Place your actual results next to your targets in a simple table. The distance between them is your gap. A gap in gross margin points to pricing or cost issues. A gap in cash flow points to timing, collections, or spending patterns.

-

Analyze root causes. A gap is a symptom. The root cause is what you fix. Common causes include cash timing mismatches (revenue arrives late, expenses arrive on time), cost creep (small expenses that grow unnoticed), and receivables delays (customers paying in 60 days when your terms say 30).

| Gap area | Common root cause | Where to look |

|---|---|---|

| Cash flow shortfall | Receivables delays, timing mismatch | AR aging report, cash flow statement |

| Shrinking gross margin | Rising supplier costs, underpricing | Income statement, cost of goods detail |

| High debt ratio | Overreliance on credit lines | Balance sheet, loan schedules |

| Low operating margin | Overhead creep, staffing costs | Operating expense breakdown |

Pro Tip: Run your gap analysis at the end of each quarter, not just at year-end. Quarterly reviews give you time to course-correct before a small gap becomes a crisis.

What financial blind spots hide your real gaps?

Financial blind spots are risks embedded in your business that do not show up clearly on any single report. Blind spots silently erode margins, stretch cash, and cause misalignment before they become visible problems. They are more dangerous than named risks because you are not watching for them.

The most common blind spots for small business owners include:

- Cash flow timing mismatch: your P&L shows profit, but your bank account is empty because revenue and expenses do not land at the same time

- Unit economics at scale: a product or service that is profitable at low volume may lose money as you grow, because fixed costs do not scale the same way revenue does

- Revenue concentration: when one or two clients represent more than 30% of your revenue, losing one creates a funding shortfall that no budget can absorb quickly

- Cost-free decisions: hiring, adding software subscriptions, or expanding a product line all carry hidden costs that rarely appear in the original decision

Maintaining a financial blind spot register is a best practice that proactively catalogs unknown risks embedded in your P&L, pricing, or hiring plans before they turn into crises. Review it quarterly and update it whenever you make a significant business decision.

A quarterly blind spot audit takes less than two hours. Pull your P&L, your cash flow statement, and your customer revenue breakdown. Ask: what would hurt us most if it changed? That question surfaces risks you are currently ignoring. Scenario stress testing, where you model what happens if your top client leaves or your supplier raises prices by 20%, turns abstract risk into a concrete number you can plan around.

How to track cash flow and find funding shortfalls

Weekly cash flow tracking is the single most effective habit for catching problems before they compound. Monthly reviews are too slow. By the time a monthly report shows a problem, you have already lost three or four weeks of response time.

Roughly 33% of failed companies cited running out of cash as a primary cause, and most of those failures came from small, unmonitored leaks rather than one large event. That means the problem was preventable with better monitoring.

A practical weekly cash flow process looks like this:

- Record all cash inflows: payments received, not invoices sent

- Record all cash outflows: every payment made, including subscriptions, payroll, and vendor payments

- Update your 13-week rolling cash flow forecast every week, adjusting for actual results

- Flag any week where projected cash falls below your minimum operating reserve

Late payments and unnoticed cost creep are leading causes of cash flow problems in profitable businesses. A client who pays 45 days late instead of 30 does not feel like a crisis. Multiply that across five clients and you have a working capital gap that forces you onto a credit line.

Monitoring accounts receivable aging weekly closes this gap fast. When an invoice hits 35 days with no payment, send a follow-up the same day. A 13-week rolling forecast updated weekly is the standard recommendation for catching timing gaps early. Pair that with bookkeeping practices that separate operating cash from reserves, and you will spot funding shortfalls weeks before they become emergencies.

Pro Tip: Set a cash floor, a minimum balance you will not let your account drop below. When you approach it, that is your trigger to review spending and accelerate collections immediately.

Automating cash flow alerts through your accounting software adds another layer of protection. Most platforms let you set threshold notifications so you get an alert when your balance drops below a set amount. That removes the human error of forgetting to check.

Key Takeaways

Identifying financial gaps requires consistent review of multiple statements, not just your profit number, because cash flow and profitability tell different stories about the same business.

| Point | Details |

|---|---|

| Use all three statements | Review your balance sheet, income statement, and cash flow statement together every quarter. |

| Analyze 8–12 quarters | Single-period reviews miss trends; multi-quarter analysis filters out seasonal noise. |

| Run a formal gap analysis | Compare actual metrics to specific targets and trace every gap back to its root cause. |

| Audit for blind spots | Quarterly blind spot reviews catch risks that standard reports do not show. |

| Track cash flow weekly | Weekly monitoring catches funding shortfalls and leaks before they become crises. |

What I have learned from watching businesses miss their own warning signs

Financial distress usually follows a slow drift pattern, with cash tightening gradually and reporting quality slipping quietly, until the owner realizes the problem is severe. I have seen this happen to businesses that were growing. Revenue was up, the team was expanding, and the owner felt confident. But cash was tighter every month, and nobody was asking why.

The uncomfortable truth is that growth can mask financial gaps. When revenue rises, it is easy to assume everything is working. What you do not see is that margins are compressing, receivables are stretching, and overhead is climbing faster than revenue. By the time those trends show up clearly, you have already lost months of runway.

The businesses that catch these problems early share one habit: they look at both profitability and cash flow together, every single month. Overreliance on profit alone is misleading. Profit tells you what you earned. Cash flow tells you what you can actually spend. You need both numbers to make a sound decision.

My strongest recommendation is to build a financial review rhythm and protect it. Put it on the calendar. Treat it like a client meeting. If you do not have the time or the expertise to run that review yourself, bring in external financial leadership. A virtual accountant or fractional CFO gives you the outside perspective that internal teams often miss. The cost of that support is almost always less than the cost of a gap you did not catch.

— Kelli

How Kelliworks helps small businesses close financial gaps

Small business owners rarely lack ambition. What they often lack is the financial visibility to act on it confidently.

Kelliworks operates as a full-service virtual accounting department built specifically for small businesses. We handle bookkeeping, tax preparation, and financial consulting so you have clean, current numbers every time you need to make a decision. Our team specializes in cash flow management, budget variance analysis, and identifying the gaps that standard bookkeeping misses. If you are ready to get a clear picture of your financial health and a plan to improve it, learn more about hiring a virtual accountant and what that looks like for a business at your stage.

FAQ

What does it mean to identify financial gaps in business?

Identifying financial gaps means measuring the difference between your current financial performance and your stated financial goals. The process covers cash flow, profitability, liquidity, and operational efficiency.

How often should I assess my business finances?

Review your key financial metrics monthly and conduct a full gap analysis quarterly. Weekly cash flow tracking is the standard for catching timing issues before they affect your operations.

Can a profitable business still have financial gaps?

Yes. Profitability and cash flow are separate measures. A business can show strong net income while running short on cash due to receivables delays or poor timing between income and expenses.

What is the fastest way to find a funding shortfall?

Build a 13-week rolling cash flow forecast and update it every week. This process surfaces funding shortfalls weeks before they appear in your bank account, giving you time to act.

What are the most common financial blind spots for small businesses?

The most common blind spots are cash flow timing mismatches, revenue concentration in one or two clients, and cost creep from small recurring expenses that grow unnoticed over time.